Salam,

Saya akan buka booth untuk CIMB Wealth Advisors dan produk-produk yang dikendalikan oleh CWA Berhad.

Maklumat lengkap adalah seperti di bawah:

Tempat : TNB Bangi

Masa : 10am -4pm.

Tarikh : 7 - 8 December 2011

Produk : CIMB Unit Trust (Award Winning and Best Islamic

Equity Fund) dan AIA AFG Takaful (Life Takaful,

Unlimited Family Medical Card, Savings Plan)

No Phone: 019-3330342.

Bagi anda yang berada berhampiran kawasan Bangi dan kawasan sekitarnya, boleh lah datang untuk sesi pencerahan terhadap produk-produk di atas.

Ahad, 4 Disember 2011

Jumaat, 18 November 2011

Rhb Asset Management Sdn Bhd. Retiring in Style

Posted on 17 November 2011 - 02:18pm

PEOPLE want to be able to spend their golden years comfortably, but often underestimate the many complex issues related to retirement, which often go beyond the financial.

Tan Beng Wah, chief executive officer of CIMB Wealth Advisors Bhd (CWA), spoke to theSunrecently about what retirement means in today’s world. His first observation is that most people are underprepared for retirement, due to several misconceptions, or ‘disconnects’.

“If you look at the current environment, there are some fundamental disconnects,” he said. “As you progress in life, most people generally improve in terms of their income, whether they are businessmen or employees; by the time you retire, your income is much higher, and therefore, you will be enjoying a different lifestyle.

“You would hope that when you retire, you will be able to enjoy a similar sort of lifestyle, but unfortunately, most people’s retirement savings is from the EPF, which is a proportion of their income.”

Very few people think about having alternate forms of retirement funds, and although more people are beginning to realise they should have additional savings, they tend to have unrealistic expectations about the amount they need to keep aside in order to retire comfortably.

“Let’s say someone thinks they can retire on RM5,000 a month in Kuala Lumpur,” Tan said. “Okay, but if this person is 30, and wants to retire at 40; that’s 10 years from now. Then you ask them how much they are willing to put aside every month for their retirement fund, and it turns out to be RM500.

“RM500 must transform into RM5,000 a month within 10 years. Can you see the problem there?”

While this is an extreme example, it does embody the attitude of many people out there.

Tan also says people rely too much on their EPF savings, not realising that they will probably outlive their savings. “EPF was set up in 1951 when the average lifespan was 55 years, meaning that you retire, and then you would have money to live comfortably for a few more years.

“Today, our lifespan average is 75 years for men, 79 for women. Hence, the savings that you have should be enough to accommodate another 20 to 25 years of living, which is where the reality is. It’s a huge problem.”

The youth mindset

The reason for the disconnect, according to Tan, is easy to pinpoint. “It’s the fault of the parents!” he exclaims. “Even children of today who don’t come from very high income families have never wanted, have never gone hungry. Whatever they want, they will get.”

Because of this, not many young people today understand the value of savings and often do not have any.

“We’ve created a generation of children that are not very independent, and who expect to be taken care of. It’s the fault of the parents, not the children. They were brought up in that environment and therefore they don’t think of their future.”

This sort of mindset often makes it challenging to get young people to understand that they have to save first before they can start spending.

The rising cost of living and currency inflation have also contributed to money losing its value compared to one generation ago.

“Take someone earning a salary of RM3,000. You ask them to save 10%, that’s RM300, it’s a huge sacrifice for them. But if you look at it, what can that RM300 buy today? So they get very discouraged. But nevertheless, the reality is that if you don’t save that RM300, you won’t save anything.”

According to Tan, a good rule of thumb is that people should have at least six months’ salary in savings. Anything beyond that, they can begin to look into investments to grow their wealth.

“There are so many ways excess cash can be invested, in order to grow their wealth for the future,” Tan says. “The issue is, how much risk is a person willing to take. But in general, young people can take more risks.

“And as to how much a person should set aside for investment, it’s entirely what they are willing to put aside.

This is what we call ‘opportunity costs’; if I invest or save this amount, then I’m giving up the opportunity to spend it on something else.”

Important questions

There are several important questions to be asked when people want to determine how much they need to retire.

Firstly, when do they want to retire? For some people, it might be at age 55, while others want to retire at 40, or believe they can work until they are 60.

However, they should also consider the second question: how long do they expect to live after their retirement? They will need to be able to support themselves during those interim years using their retirement fund.

Thirdly, what sort of lifestyle do they want to lead after retirement? Most want to be able to enjoy themselves fully, travelling the world or pursuing their lifelong interests.

But they should also consider other issues, including their health and their social network of friends.

To Tan, the most important aspect of planning for retirement is going beyond the numbers. “This country has a lot of problems when dealing with retirement,” he said.

“Retirement and ageing go beyond money. The qualitative and quantitative have to be considered together. You can’t just talk about the material aspects, and not talk about the social aspects and quality of life.

“I wish that people talked more about these kind of things, and not just ask about the numbers.”

Rabu, 12 Oktober 2011

MAAKL Mutual Berhad. 41 Belia Muflis Setiap Hari Gagal Urus Kewangan

Dari Utusan Malaysia 12/10/2011

KUALA LUMPUR 11 Okt. - Seramai 41 belia Malaysia berumur lingkungan 21 hingga 40 tahun dianggarkan menjadi muflis setiap hari akibat kurangnya pengetahuan berkaitan pengurusan kewangan.

Ketua Pegawai Eksekutif Gabungan Persatuan Pengguna Malaysia (FOMCA), Datuk Paul Selva Raj berkata, belia merupakan golongan utama menghadapi masalah kewangan dan menjadi muflis berbanding orang dewasa akibat daripada perbelanjaan yang tidak terkawal.

"Antara punca utama adalah kerana urusan sewa beli seperti kereta, rumah dan penggunaan kad kredit.

"Apabila lebih 30 peratus daripada gaji bulanan digunakan untuk membayar hutang, seseorang itu sudah dikira mempunyai masalah kewangan.

"Ini menunjukkan betapa kurangnya kesedaran golongan muda berkaitan pengurusan kewangan mereka dan jika perkara ini dibiarkan, ia akan menjadi lebih teruk," katanya pada sidang akhbar selepas majlis pelancaran program RINGGIT Pertama Saya di sini, hari ini.

Program RINGGIT Pertama Saya adalah kerjasama antara Persatuan Pendidikan dan Penyelidikan Pengguna Malaysia (ERA Consumer) dan Citibank Bhd. dalam usaha memupuk kesedaran kanak-kanak berhubung pentingnya pengurusan kewangan.

Program ini melibatkan 400 kanak-kanak berusia antara empat hingga enam tahun dari 20 buah tadika di seluruh negara.

Paul menambah, FOMCA menggesa kerajaan untuk memasukkan pendidikan pengurusan kewangan di dalam sistem persekolahan untuk memberi ilmu bersesuaian kepada kanak-kanak.

"Kita harus mendidik generasi akan datang mengenai pentingnya pengurusan kewangan dan usaha ini sebaiknya dimulakan dari peringkat sekolah lagi," ujarnya.

INVEST SEKARANG DENGAN MENGISI FORM DI SINI.

KUALA LUMPUR 11 Okt. - Seramai 41 belia Malaysia berumur lingkungan 21 hingga 40 tahun dianggarkan menjadi muflis setiap hari akibat kurangnya pengetahuan berkaitan pengurusan kewangan.

Ketua Pegawai Eksekutif Gabungan Persatuan Pengguna Malaysia (FOMCA), Datuk Paul Selva Raj berkata, belia merupakan golongan utama menghadapi masalah kewangan dan menjadi muflis berbanding orang dewasa akibat daripada perbelanjaan yang tidak terkawal.

"Antara punca utama adalah kerana urusan sewa beli seperti kereta, rumah dan penggunaan kad kredit.

"Apabila lebih 30 peratus daripada gaji bulanan digunakan untuk membayar hutang, seseorang itu sudah dikira mempunyai masalah kewangan.

"Ini menunjukkan betapa kurangnya kesedaran golongan muda berkaitan pengurusan kewangan mereka dan jika perkara ini dibiarkan, ia akan menjadi lebih teruk," katanya pada sidang akhbar selepas majlis pelancaran program RINGGIT Pertama Saya di sini, hari ini.

Program RINGGIT Pertama Saya adalah kerjasama antara Persatuan Pendidikan dan Penyelidikan Pengguna Malaysia (ERA Consumer) dan Citibank Bhd. dalam usaha memupuk kesedaran kanak-kanak berhubung pentingnya pengurusan kewangan.

Program ini melibatkan 400 kanak-kanak berusia antara empat hingga enam tahun dari 20 buah tadika di seluruh negara.

Paul menambah, FOMCA menggesa kerajaan untuk memasukkan pendidikan pengurusan kewangan di dalam sistem persekolahan untuk memberi ilmu bersesuaian kepada kanak-kanak.

"Kita harus mendidik generasi akan datang mengenai pentingnya pengurusan kewangan dan usaha ini sebaiknya dimulakan dari peringkat sekolah lagi," ujarnya.

INVEST SEKARANG DENGAN MENGISI FORM DI SINI.

Sabtu, 8 Oktober 2011

MAAKL Mutual Berhad. Bursa goes into rebound mode

From : http://www.btimes.com.my/Current_News/BTIMES/articles/08technically/Article/

SHARE prices on Bursa Malaysia staged follow-through rebounds for the week ended yesterday. The local market remained firm when it moved in sync with Wall Street and the Hong Kong stock market.

The FBM Kuala Lumpur Composite Index (FBM KLCI) posted a week-on-week gain of 12.92 points, or 0.93 per cent, for the week ended yesterday. It stayed marginally above its immediate downside support of 1,400 over the week.

Bursa consolidated in tandem with the technical pullbacks on the Hong Kong and Tokyo stock markets on Monday. The FBM KLCI opened at 1,381.81 before hitting its day low of 1,353.45. It closed at 1,367.52, recording a day-on-day loss of 19.61 points, or 1.41 per cent.

Share prices on Bursa Malaysia consolidated for the second trading day on Tuesday, in tune with the market pullbacks on regional stock markets. The FBM KLCI trended between its day low of 1,356.77 and day high of 1,375.02. It ended at 1,356.77, recording another day-on-day loss of 10.75 points, or 0.79 per cent.

After a mild rebound on the Wall Street on Tuesday, the FBM KLCI rebounded in earnest on Wednesday. The FBM KLCI ended the day at 1,375.67, posting a day-on-day gain of 18.90 points, or 1.39 per cent.

The index continued to rebound further on Thursday. It trended between day low of 1,381.17 to a day high of 1,395.28 before closing at 1,393.69, recording another day-on-day gain of 18.02 points, or 1.31 per cent.

Despite the sharp rebound on Wall Street, the FBM KLCI only managed to climb the day high of 1,4002.58 yesterday before easing marginally to close at 1,400.05, giving a day-on-day gain of 6.36 points, or 0.46 per cent.

The FBM KLCI staged a follow-through technical rebound for the second consecutive week. It rebounded to close at 1,400.05 yesterday, giving a week-on-week gain of 12.92 points, or 0.93 per cent.

The FTSE Bursa Malaysia Small Cap Index gained 81.71 points, or 0.79 per cent, to close at 10,478.45 while the FTSE Bursa Malaysia ACE Index advanced 49.91 points, or 1.39 per cent, to 3,647.86 level yesterday.

The following are the readings of some of the FBM KLCI's technical indicators:

Moving Averages: The FBM KLCI continued to stay below the support of all of its 30-, 50-, 100- and 200-day moving averages. It had since stayed above the support of its 10- and 20-day moving averages.

Momentum Index: Its short-term momentum index continued to trend below its neutral reference line at the market close yesterday.

On Balance Volume: Its short-term OBV trend stayed above the support of its 10-day exponential moving averages.

Relative Strength Index: Its 14-day RSI stood at the 46.35 per cent level yesterday.

Outlook

The FBM KLCI hit its week low of 1,353.45 on Monday, staging a successful re-test of the confines of this column's envisaged support zone (1,349 to 1,383 levels).

Subsequently, the FBM KLCI rebounded to its week high of 1,402.58 yesterday, moving into the confines of this column's envisaged resistance zone (1,390 to 1,425 levels).

A quick review of the performances of the FBM KLCI's 30 components, losers outpaced gainers by 16 to 14. Tenaga, Axiata, Maybank and IOI Corp's combined gains of 21-sen, 19-sen, 18-sen and 17-sen respectively accounted for the bulk of the FBM KLCI's week-on-week gain of 12.92 points, or 0.93 per cent.

Petronas Dagangan Bhd (Petdag) remained as the week's top performing component to-date with a total year-to-date gain of RM4.40, or 37.61 per cent.

The FBM KLCI's weekly chart continued to stay below its intermediate-term uptrend support (See FBM KLCI's weekly chart - A3:A4) during the week. It also continued to stay below the support of its immediate downside support (A1:A2) last week. It staged another successful re-test of its next support (A5:A6).

Chartwise, the FBM KLCI breached its immediate downside support (See FBM KLCI's daily chart - B5:B6) on September 15 and continued to stay below it on September 23. With that, the FBM KLCI had since stayed below its two trendlines (B3:B4 and B5:B6) last week. The FBM KLCI staged a successful re-test of its downside support (B7:B8) on September 26 before rebounding to close at 1,400.05 points yesterday.

The FBM KLCI's weekly and monthly fast MACDs (moving average convergence divergence) continued to stay below their respective slow MACDs yesterday. Its daily fast MACD had since stayed above daily slow MACD.

The FBM KLCI's 14-day RSI stayed at 46.34 per cent level yesterday. Its 14-week and 14-month RSI stayed at 34.38 and 50.54 levels respectively.

Last week, this column commented that the FBM KLCI might stage another attempt in trying to crack its immediate overhead resistance of 1,400. It did. The FBM KLCI closed at 1,400.05 yesterday.

Against the backdrop of rebounds on the Wall Street and regional stock markets during the week, there is an even chance that these markets will remain in their rebound mood. With that, the FBM KLCI is likely to stage yet another follow-through rebound.

Next week, the FBM KLCI's envisaged resistance zone is at the 1,404 to 1,438 levels while its immediate downside support is at the 1,362 to 1,396 levels.

The subject expressed above is based on technical analysis and opinions of the writer. It is not a solicitation to buy or sell.

Read more: Bursa goes into rebound mode http://www.btimes.com.my/Current_News/BTIMES/articles/08technically/Article/#ixzz1aB7yqzY8

SHARE prices on Bursa Malaysia staged follow-through rebounds for the week ended yesterday. The local market remained firm when it moved in sync with Wall Street and the Hong Kong stock market.

The FBM Kuala Lumpur Composite Index (FBM KLCI) posted a week-on-week gain of 12.92 points, or 0.93 per cent, for the week ended yesterday. It stayed marginally above its immediate downside support of 1,400 over the week.

Bursa consolidated in tandem with the technical pullbacks on the Hong Kong and Tokyo stock markets on Monday. The FBM KLCI opened at 1,381.81 before hitting its day low of 1,353.45. It closed at 1,367.52, recording a day-on-day loss of 19.61 points, or 1.41 per cent.

Share prices on Bursa Malaysia consolidated for the second trading day on Tuesday, in tune with the market pullbacks on regional stock markets. The FBM KLCI trended between its day low of 1,356.77 and day high of 1,375.02. It ended at 1,356.77, recording another day-on-day loss of 10.75 points, or 0.79 per cent.

After a mild rebound on the Wall Street on Tuesday, the FBM KLCI rebounded in earnest on Wednesday. The FBM KLCI ended the day at 1,375.67, posting a day-on-day gain of 18.90 points, or 1.39 per cent.

The index continued to rebound further on Thursday. It trended between day low of 1,381.17 to a day high of 1,395.28 before closing at 1,393.69, recording another day-on-day gain of 18.02 points, or 1.31 per cent.

Despite the sharp rebound on Wall Street, the FBM KLCI only managed to climb the day high of 1,4002.58 yesterday before easing marginally to close at 1,400.05, giving a day-on-day gain of 6.36 points, or 0.46 per cent.

The FBM KLCI staged a follow-through technical rebound for the second consecutive week. It rebounded to close at 1,400.05 yesterday, giving a week-on-week gain of 12.92 points, or 0.93 per cent.

The FTSE Bursa Malaysia Small Cap Index gained 81.71 points, or 0.79 per cent, to close at 10,478.45 while the FTSE Bursa Malaysia ACE Index advanced 49.91 points, or 1.39 per cent, to 3,647.86 level yesterday.

The following are the readings of some of the FBM KLCI's technical indicators:

Moving Averages: The FBM KLCI continued to stay below the support of all of its 30-, 50-, 100- and 200-day moving averages. It had since stayed above the support of its 10- and 20-day moving averages.

Momentum Index: Its short-term momentum index continued to trend below its neutral reference line at the market close yesterday.

On Balance Volume: Its short-term OBV trend stayed above the support of its 10-day exponential moving averages.

Relative Strength Index: Its 14-day RSI stood at the 46.35 per cent level yesterday.

Outlook

The FBM KLCI hit its week low of 1,353.45 on Monday, staging a successful re-test of the confines of this column's envisaged support zone (1,349 to 1,383 levels).

Subsequently, the FBM KLCI rebounded to its week high of 1,402.58 yesterday, moving into the confines of this column's envisaged resistance zone (1,390 to 1,425 levels).

A quick review of the performances of the FBM KLCI's 30 components, losers outpaced gainers by 16 to 14. Tenaga, Axiata, Maybank and IOI Corp's combined gains of 21-sen, 19-sen, 18-sen and 17-sen respectively accounted for the bulk of the FBM KLCI's week-on-week gain of 12.92 points, or 0.93 per cent.

Petronas Dagangan Bhd (Petdag) remained as the week's top performing component to-date with a total year-to-date gain of RM4.40, or 37.61 per cent.

The FBM KLCI's weekly chart continued to stay below its intermediate-term uptrend support (See FBM KLCI's weekly chart - A3:A4) during the week. It also continued to stay below the support of its immediate downside support (A1:A2) last week. It staged another successful re-test of its next support (A5:A6).

Chartwise, the FBM KLCI breached its immediate downside support (See FBM KLCI's daily chart - B5:B6) on September 15 and continued to stay below it on September 23. With that, the FBM KLCI had since stayed below its two trendlines (B3:B4 and B5:B6) last week. The FBM KLCI staged a successful re-test of its downside support (B7:B8) on September 26 before rebounding to close at 1,400.05 points yesterday.

The FBM KLCI's weekly and monthly fast MACDs (moving average convergence divergence) continued to stay below their respective slow MACDs yesterday. Its daily fast MACD had since stayed above daily slow MACD.

The FBM KLCI's 14-day RSI stayed at 46.34 per cent level yesterday. Its 14-week and 14-month RSI stayed at 34.38 and 50.54 levels respectively.

Last week, this column commented that the FBM KLCI might stage another attempt in trying to crack its immediate overhead resistance of 1,400. It did. The FBM KLCI closed at 1,400.05 yesterday.

Against the backdrop of rebounds on the Wall Street and regional stock markets during the week, there is an even chance that these markets will remain in their rebound mood. With that, the FBM KLCI is likely to stage yet another follow-through rebound.

Next week, the FBM KLCI's envisaged resistance zone is at the 1,404 to 1,438 levels while its immediate downside support is at the 1,362 to 1,396 levels.

The subject expressed above is based on technical analysis and opinions of the writer. It is not a solicitation to buy or sell.

Read more: Bursa goes into rebound mode http://www.btimes.com.my/Current_News/BTIMES/articles/08technically/Article/#ixzz1aB7yqzY8

Online form powered by 123ContactForm.com | Report abuse

Sabtu, 17 September 2011

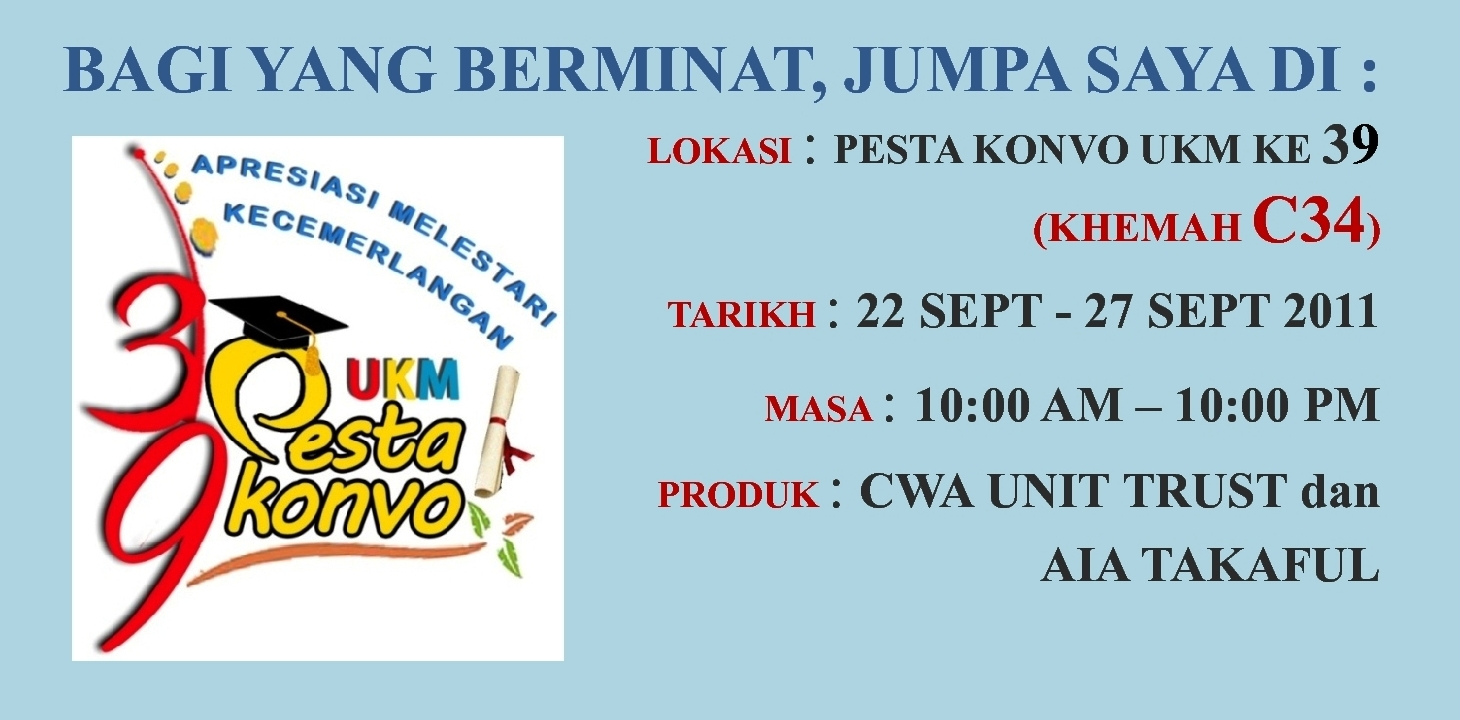

Booth di Pesta Konvo UKM ke 39

Bagi yang tinggal berhampiran Bangi atau yang melawati Pesta Konvo UKM boleh berjumpa saya untuk mengetahui lebih lanjut tentang produk2 yang ditawarkan oleh CIMB Wealth Advisors Berhad.

Rabu, 14 September 2011

A-Excel, Menyimpan Sambil Melindungi Diri Anda.

A-Excel

Pelan Perlindungan dan Simpanan

Impian kewangan anda tidak pernah terhenti walaupun anda melangkah ke fasa hidup yang berbeza. Menyimpan untuk impian kewangan anda adalah mudah sekiranya anda merancang kewangan anda terlebih dahulu dan dengan menyediakan wang sampingan tetap untuk rancangan tersebut. Memperkenalkan A-Excel, penyelesaian kewangan lengkap yang menggabungkan perlindungan takaful dan simpanan dalam satu pelan. A-Excel boleh membantu anda mencapai impian kewangan anda seperti tanggungan pendidikan anak-anak, modal untuk perniagaan sendiri ataupun persediaan untuk persaraan.

Apakah itu A-Excel?

A-Excel adalah pelan takaful caruman tetap yang akan matang di hujung tahun ke 20 sijil dengan bayaran caruman selama 20 tahun. la menyedíakan perlindungan takaful diatas kematian ataupun orang dilindungi mengalami hilang upaya menyeluruh dan kekal.

Contoh : Jika anda mengambil perlindungan (sum covered) RM200K, maka setiap 2 tahun anda akan mendapat RM20K. Sehingga tahun ke 20. Atau perlindungan min RM30K anda boleh mendapatkan RM3K setiap 2 tahun secara konsisten.

FAEDAH

Apakah perlindungan faedah yang disediakan?

Pelan ini menyediakan:

Faedah Kematian

Sekiranya berlaku kematian orang dilindungi sebelum tarikh matang sijil dan semasa sijil masih berkuatkuasa, jumlah perlindungan asal dan nilai di dalam akaun peserta ("Nilai Akaun Peserta") akan dibayar. Sekiranya orang dilindungi adalah kanak-kanak, jumlah perlindungan asal yang akan dibayar adalah berdasarkan Peratusan Lien Juvenil seperti yang ditunjukkan seperti dibawah:

Kurang dari 1 tahun 20%

1 tahun 40%

2 tahun 60%

3 tahun 80%

4 tahun atau ke atas 100%

Faedah Hilang Upaya Menyeluruh dan Kekal (TPD)

Sekiranya anda hilang upaya menyeluruh dan kekal sebelum umur 60 tahun, Nilai Akaun Peserta berserta jumlah sekaligus yang didahulukan sama ada bersamaan dengan 100% jumlah perlindungan TPD atau 10% dari jumlah perlindungan TPD untuk tempoh dua(2) tahun pertama, diikuti dengan baki 80% pada tahun ketiga, bergantung kepada punca kehilangan upaya tersebut, akan dibayar.

Faedah Kematangan

Nilai Akaun Peserta akan dibayar jika sijil masih berkuatkuasa dan orang yang dilindungi masih hidup semasa tarikh matang.

Adakah saya dibenarkan untuk melampirkan sebarang rider ke pelan ini?

Anda boleh memilih untuk meningkatkan lagi perlindungan takaful anda dengan menambahkan perlindungan tambahan yang terdiri daripada pelbagai pilihan faedah kami dibawah:

1) Faedah Kehidupan

Kami akan membayar anda Faedah Kehidupan sebanyak 10% darijumlah perlindungan asal pada setiap penghujung dua (2) tahun sijil sehingga sijil anda matang. Anda boleh memilih untuk menerima Faedah Kehidupan tersebut ataupun menyimpannya dengan kami untukmenerima keuntungan yang akan dikongsi di antara Pengendali Takaful dan anda dengan nisbah 20:80.

Secara ringkasnya, setiap 2 tahun anda boleh keluarkan 10% dari jumlah asal. Sekiranya anda membeli jumlah RM30000, maka setiap 2 tahun boleh keluarkan RM3000.

2) Penepian Caruman Penyakit Kritikal

Mengenepikan dan membayar caruman tetap sijil asas dan Faedah Kehidupan (jika dilampirkan) atas nama peserta sekiranya orang dilindungi didiagnosiskan menghidap penyakit kritikal yang tertentu atau menjalani sebarang pembedahan yang dilindungi.

3)Faedah Pencarum (CB) dan Faedah Pencarum untuk Penyakit Kritikal (CB-CI)

Sekiranya pencarum meninggal dunia, hilang upaya menyeluruh dan kekal atau didiagnosiskan menghidap penyakit kritikal atau menjalani pembedahan untuk salah satu dari 35 penyakit kritikal fiika CB-CI dilampirkan) seperti yang tersenarai di dalam sijil takaful, sebelum pencarum mencapai umur 60 tahun ataupun tarikh tamat rider, yang mana terdahulu,

semua caruman akan datang untuk sijil asas dan Faedah Kehidupan (jika dilampirkan) tidak perlu dibayar sehingga kanak-kanak tersebut mencapai umur 25 tahun.

KELAYAKAN

Adakah saya layak memohon A-Excel?

Pelan ini boleh disertai oleh individu yang berumur diantara umur 4 minggu hingga 65 tahun, tertakluk kepada kelulusan pengunderaitan kami.

JUMLAH PERLINDUNGAN

Berapakah jumlah perlindungan minimum?

RM30,000

CARUMAN

Berapa lamakah tempoh bayaran caruman bagi A-Excel?

Caruman perlu dibayar selama 20 tahun sijil ataupun sehingga kematian orang dilindungi, yang mana terdahulu.

KLIK SINI UNTUK DAPATKAN PROPOSAL PERCUMA

Sabtu, 27 Ogos 2011

Selamat Hari Raya Aidilfitri

Sempena Hari Raya ini saya ingin mengucapkan Selamat Hari Raya Aidilfitri, maaf zahir dan batin kepada para pembaca dan juga kepada klien2 saya dari Unit Trust dan juga Takaful. Kalau balik kampung tu pastikan anda memandu berhati-hati, patuhi undang-undang jalan raya dan elakkan dari memberi duit saman raya .

Selamat Hari Raya Aidilfitri. Maaf Zahir dan Batin.

P/S: bagi yang berminat untuk mendapatkan polisi takaful dan melabur dalam unit trust boleh hubungi saya untuk maklumat lanjut. walaupun raya, servis adalah seperti biasa.

Selamat Hari Raya Aidilfitri. Maaf Zahir dan Batin.

P/S: bagi yang berminat untuk mendapatkan polisi takaful dan melabur dalam unit trust boleh hubungi saya untuk maklumat lanjut. walaupun raya, servis adalah seperti biasa.

Sabtu, 13 Ogos 2011

The Best Medical Card : Takaful A-Medik Unlimited Medical Card

Instead of asking "Why were we born?", "What were we born for" maybe we should just keep in mind "for whom do we live"...

Bagaimana Takaful A-Medik Membantu Pelan Perancangan Kewangan Anda?

Dengan Takaful, perancangan perbelanjaan perubatan boleh dilakukan dengan lebih cekap. Kalau ada 6 orang anak, anda tak perlu belikan 6 polisi untuk anak2 anda. Tapi 1 POLISI UNTUK SELURUH KELUARGA ANDA. JIMAT, KAN?

Takaful A-Medik Medical Card.

Perbelanjaan perubatan yang kian meningkat akan menjejaskan simpanan anda jika berlakunya penghospitalan atau pembedahan. Dengan A-Medik, kami boleh membantu anda untuk mencegah kemerosotan kewangan kerana pelan ini menawarkan perlindungan perubatan yang komprehensif sehingga umur 99 tahun. Selain itu, pelan ini juga menawarkan had jumlah keseluruhan seumur hidup yang tidak terbatas bagi setiap orang dilindungi di mana anda tidak perlu bimbang akan kekurangan pembayaran balik perubatan dalam jangka masa yang panjang.

Oleh itu, anda dapat menumpukan perhatian untuk meningkatkan simpanan anda tanpa perlu bimbang akan penyusutan simpanan disebabkan kejadian yang tidak diduga.

Apakah itu A-Medik?

A-Medik adalah pelan perubatan caruman tetap yang meliputi kos penghospitalan dan

pembedahan dalam keadaan penghospitalan kerana sakit atau punca kemalangan. Pelan ini menyediakan faedah tambahan yang boleh dilampirkan bersama pelan-pelan takaful keluarga dan takaful berkaitan-pelaburan.

AMAUN PERLINDUNGAN

Bolehkah saya memperluaskan amaun perlindungan kepada ahli keluarga saya di dalam pelan ini?

Anda mempunyai pilihan untuk memperluaskan perlindungan ini kepada ahli keluarga anda. Tiga (3) pelan keluarga yang disediakan adalah:

(i) Orang Dilindungi + Pasangan

(ii) Orang Dilindungi + Keluarga

(iii) Orang Dilindungi + Anak

Dalam pelan keluarga, semua ahli keluarga yang dilindungi dalam satu sijil akan dilindungi dengan amaun yang sama.

Adakah saya perlu menanggung sebarang perbelanjaan untuk penghospitalan?

Perbelanjaan layak yang melebihi Amaun Bebas Ko-Takaful adalah tertakluk kepada Amaun Ko-Takaful sebanyak RM3,000 atau 10% daripada baki yang melebihi Amaun Bebas Ko-Takaful, mana-mana yang lebih rendah.

Bagaimana Takaful A-Medik Membantu Pelan Perancangan Kewangan Anda?

Bagi yang masih bujang, sekarang adalah masa yang sesuai untuk membuat perancangan jangka panjang. Di Takaful, perancangan Medical Card boleh dibuat ketika anda masih bujang hingga anda mempunyai ramai anak.

Ketika Bujang : Medical Card Individu

Ketika Baru Berkahwin(tiada anak) :Upgrade ke Medical Card Anda + Pasangan

Ketika Sudah ada anak:Upgrade ke Medical Card Keluarga atau Anda + Anak2.

Jadi, perancangan perbelanjaan perubatan anda dan keluarga anda pada masa akan datang, bermula pada hari ini. Dan mulakan dengan Takaful untuk perancangan penjimatan jangka panjang (Bukan pada hari ini sahaja) Bermula dengan Takaful Medical Card pada hari ini, memudahkan anda untuk mengubah polisi pada masa depan ketika sudah berkahwin atau mempunyai anak2.

FAEDAH

Apakah perlindungan/faedah yang disediakan?

Jadual faedah A-Medik

Rabu, 27 Julai 2011

Jadual Berbuka Puasa

A)Lembah Klang

B)Melaka

C)Negeri Sembilan

D)Johor

E)Kedah

F)Perak

G)Pahang

6)Zon 6 : Cameron Highland, Bukit Fraser, Genting Highland

H)Perlis

I)Terengganu

1)Zon 1 : Kuala Terengganu, Marang

2)Zon 2 : Besut, Setiu

3)Zon 3 : Hulu Terengganu

J)Kelantan

1)Zon 1 : Kota Bharu, Paser Putih, Bachok, Tumpat,Pasir Mas, Tanah Merah, Machang, Kuala Krai, Gua Musang.

2)Zon 2 : Jeli, Gua Musang (Galas&Bertam), Lojing

H)Perlis

I)Terengganu

1)Zon 1 : Kuala Terengganu, Marang

2)Zon 2 : Besut, Setiu

3)Zon 3 : Hulu Terengganu

J)Kelantan

1)Zon 1 : Kota Bharu, Paser Putih, Bachok, Tumpat,Pasir Mas, Tanah Merah, Machang, Kuala Krai, Gua Musang.

2)Zon 2 : Jeli, Gua Musang (Galas&Bertam), Lojing

Isnin, 11 Julai 2011

FBM KLCI may test 1,600 barrier

KUALA LUMPUR: Bursa Malaysia might test the psychological important 1,600-point level for the first time in its history this week.

"At current levels, the market certainly needs more good news to sustain the rise," said an analyst.

Technically, the local market continues to paint a bullish landscape, with the key index turning sideways this week, pending a clearer picture to emerge.

To the upside, stiff resistance is maintained at the 1,585-1,600 points band. Thereafter, Bursa Malaysia is expected to encounter significant challenges at every 20 or 30 points interval.

Near-term sentiment will hinge on the soon-to-be-released financial sector master plan, results of the Economic Transformation Programme tender outs and banking mergers.

Elsewhere, Portugal's sovereign debt, the US debt ceiling, Thailand's new regime's policies and China's interest rate cycle will also be on the investor radar.

Last week, Bank Negara Malaysia decided to keep the Overnight Policy Rate at 3 per cent but raised the statutory reserve requirement from 3 per cent to 4 per cent as a measure to manage the significant build-up in liquidity.

The biggest near-term driver for local sectors would come from Japan which is recovering from the March quake faster than most economists expected.

Stocks in the limelight include banking and oil and gas such as BIMB, AFG, Petronas Dagangan and Sapura Crest due to short term holding strategies.

On a Friday-to-Friday basis, the FBM KLCI rose to 1,594.74 from 1,582.94 and the Finance Index rose 11.22 points to 15,038.74.

Weekly volume rose to 4.66 billion shares valued at RM8.63 billion from the 4.52 billion shares valued at RM8.27 billion previously.

Read more: FBM KLCI may test 1,600 barrier http://www.btimes.com.my/Current_News/BTIMES/articles/rupind/Article/#ixzz1Rmmd2UZK

INVEST SEKARANG DENGAN MENGISI FORM DI SINI.

|

Late fund buying on selected stocks pushed the index to a fresh historic close of 1,594.74-points.

The FBM KLCI continued to scale new highs on sporadic bargain hunting activity, undergoing a healthy correction in the past week.

Bursa Malaysia was firmly positive since the bulls made it to the uncharted territory, riding on the strength of overseas equities, especially Wall Street, optimism of global economy and improvement in the eurozone debt crisis.

Last Friday, the FBM KLCI closed 4.5 points higher as a result of the government's Economic Transformation Programme (ETP) and plans to loosen its shareholding in government-linked companies.

The FBM KLCI continued to scale new highs on sporadic bargain hunting activity, undergoing a healthy correction in the past week.

Bursa Malaysia was firmly positive since the bulls made it to the uncharted territory, riding on the strength of overseas equities, especially Wall Street, optimism of global economy and improvement in the eurozone debt crisis.

Last Friday, the FBM KLCI closed 4.5 points higher as a result of the government's Economic Transformation Programme (ETP) and plans to loosen its shareholding in government-linked companies.

Technically, the local market continues to paint a bullish landscape, with the key index turning sideways this week, pending a clearer picture to emerge.

To the upside, stiff resistance is maintained at the 1,585-1,600 points band. Thereafter, Bursa Malaysia is expected to encounter significant challenges at every 20 or 30 points interval.

Near-term sentiment will hinge on the soon-to-be-released financial sector master plan, results of the Economic Transformation Programme tender outs and banking mergers.

Elsewhere, Portugal's sovereign debt, the US debt ceiling, Thailand's new regime's policies and China's interest rate cycle will also be on the investor radar.

Last week, Bank Negara Malaysia decided to keep the Overnight Policy Rate at 3 per cent but raised the statutory reserve requirement from 3 per cent to 4 per cent as a measure to manage the significant build-up in liquidity.

The biggest near-term driver for local sectors would come from Japan which is recovering from the March quake faster than most economists expected.

Stocks in the limelight include banking and oil and gas such as BIMB, AFG, Petronas Dagangan and Sapura Crest due to short term holding strategies.

On a Friday-to-Friday basis, the FBM KLCI rose to 1,594.74 from 1,582.94 and the Finance Index rose 11.22 points to 15,038.74.

Weekly volume rose to 4.66 billion shares valued at RM8.63 billion from the 4.52 billion shares valued at RM8.27 billion previously.

Read more: FBM KLCI may test 1,600 barrier http://www.btimes.com.my/Current_News/BTIMES/articles/rupind/Article/#ixzz1Rmmd2UZK

INVEST SEKARANG DENGAN MENGISI FORM DI SINI.

Rabu, 15 Jun 2011

Takaful Product Line Up-Why We Need Protection?

WHY WE NEED INSURANCE PROTECTION?

Instead of asking "Why were we born?", "What were we born for" maybe we should just keep in mind "for whom do we live"...

Instead of asking "Why were we born?", "What were we born for" maybe we should just keep in mind "for whom do we live"...

- Medical expenses is No 1 factor for personal financial management failure in Malaysia.

- Medical cost increment is 15% every year.

- Secure your family's continuity of lifestyle through income replacement solution for your family.

- In case of disablement due to accident e.g. unable to work, your love ones can take care of you without worrying about additional expenses incurred.

- No need to pay huge medical cost and bills.

- Access to quality health facilities/treatment.

BUT I STILL YOUNG, WHY SHOULD I NEED INSURANCE

PROTECTION?

- The best time to buy takaful/insurance is when you are still young and healthy. Most insurance companies will not cover you if you already have any illness.

- Serious illness or accident can strike anyone any age and at any time. When it does, you would want to be able to afford the best medical care you can get.

- Takaful/insurance can help you pay for hospital room and board, doctor's fee, surgical fee, medical supplies etc. Most insurance companies offer an Assist Card facility for easy admissions to any approved panel hospitals.

- When it comes to insurance/takaful, it's always "The Sooner the Better".

WHY TAKAFUL?

- Monthly low contribution from RM100

- Medical Card yearly limits starting from RM90000. UNLIMITED FOR LIFETIME!

- Family Medical Card covers unlimited family members.

- Contribution amount is based on your last birthday not on your next birthday.That's mean cheaper.

- Additional Riders :

· Waiver of Contribution

· Critical Illness.

· Personal Accident

· Hospitalization and Surgical

AVAILABLE TAKAFUL PLAN

Protection & Investment

A-Mas

Your protection and financial needs change over time as you move towards different life stages. Introducing A-Mas, a regular contribution investment-linked takaful (ILT) protection plan that provides a comprehensive takaful coverage through a range of optional benefits. It helps you manage the changes and uncertainty in every stage of your life. This plan will also assist you to accumulate your wealth effortlessly over a long-term period. In addition, it offers you the investment flexibility where you are allowed to choose the Shariah-compliant investment funds according to your own risk appetite.

You have an option to further enhance your takaful protection by adding extra coverage from our range of optional benefits below:

- Waiver of Contribution

Waive and pay the contributions of the certificate on behalf of participant in the event the person covered is diagnosed to be suffering from a specified critical illness or total permanent disability prior to age 60. - Critical Illness

The sum covered of the critical illness benefit is payable in one lump sum upon diagnosis of a critical illness to help you coping with the extra medical cost. - Personal Accident

Coverage is provided for death or injuries resulting from an accident. - Hospitalization and Surgical

Coverage is provided by assisting you in coping with the medical expenses incurred in times of hospitalization.

Protection

A-Prima

Life is full of unexpected events and these events may be the impediments that prevent you from moving on and achieving your goals. Introducing A-Prima, a regular contribution family takaful plan that helps you manages the uncertainty and minimizes the financial ramification as a result of these unfortunate events. Hence, you can continue to pursue your dreams to achieve a better life.

You have an option to further enhance your takaful protection by adding extra coverage from our range of optional benefits below:

- Critical Illness

The sum covered of the critical illness benefit is payable in one lump sum upon diagnosis of a critical illness to help you coping with the extra medical cost. - Critical Illness Waiver of Contribution

Waive and pay the regular contribution for the basic certificate on behalf of participant in the event the person covered is diagnosed to be suffering from any one of the specified critical illness or undergoes a covered surgery. - Personal Accident

Coverage is provided for death or injuries resulting from an accident. - Hospitalization and Surgical

Coverage is provided by assisting you in coping with the medical expenses incurred in times of hospitalization.

Langgan:

Catatan (Atom)